March 2025 Jobs Report and April 2 Global Tariffs: The Fault is Not in Our Stars

Trump Escalates Trade War Past the Point of No Return; The Global Economy Will Never Be the Same

“Why, man, he doth bestride the narrow world, Like a Colossus and we petty men, Walk under his huge legs and peep about, To find ourselves dishonourable graves. Men at sometime are masters of their fates: The fault, dear Brutus, is not in our stars, But in ourselves, that we are underlings.” - Julius Caesar, Act I, Scene II

Historians often say the Roman Empire fell in 476 CE not because of conquest, but a failure of its own institutions.1 As the empire expanded and later struggled to defend its vast territory, public spending - especially on the military - skyrocketed. The state was forced to tax all citizens heavily, but the burden fell on the poor, as wealthy elites used their influence to avoid paying their fair share. To meet fiscal demands, emperors debased the currency, causing hyperinflation. Diocletian - best known for bringing stability after the Crisis of the Third Century - tried to stop it with the now infamous Edict on Maximum Prices, but failed miserably. Trade routes across the empire became more dangerous. The once-interconnected and thriving Roman market fractured into localized, subsistence economies. This left them unprepared to meet the challenges of the Visigoths in 410, the Vandals in 455, and the Germanic tribes in 476, who sacked Rome and deposed the last emperor.2

It is not hard to see parallels between the declining Roman empire and the modern day United States. Both states share fiscal imbalances, growing inequality, institutional erosion, and too much power in the hands of the head of state. But unlike Ancient Rome, the U.S. still possesses a flexible and innovative modern economy with a highly-educated workforce, a much better understanding of monetary policy, democracy with some checks and balances, and the world’s strongest army. Nevertheless, Donald Trump’s global trade war, if left unchecked, seems poised to be one of the worst self-inflicted wounds in American economic history.

A week ago, Trump announced a suite of new tariffs intended to dramatically reduce the U.S. trade deficit, re-shore manufacturing jobs, help pay down the national debt, and/or lower barriers to trade for American firms, depending on who you ask. First, a universal baseline 10 percent tariff will be applied to all imported goods entering the U.S. starting April 5th. In addition, many countries that have high trade surpluses with the U.S. - most notably China, the European Union, and Japan - are being subjected to “reciprocal” tariffs on top of the universal 10 percent from April 9th. He’s even going after the penguins!

While in theory these tariffs were designed to match levies and unfair trade practices from other countries, in practice they were calculated using an embarrassingly simple formula3 described on the U.S. Office of the Trade Representative’s website.

In this formula, x stands for exports to and m for imports from a given country. Epsilon is set equal to 4, and varphi is equal to 0.25.4 For example, China’s reciprocal tariff rate is calculated by taking the U.S. trade deficit in goods with China, and dividing it by two times total goods imports from China. The goods trade deficit was $295.4 billion, and total Chinese imports were $427.2 billion. Divide the former by the latter, and you get roughly 0.67. Divide that by two, and you get 0.335, or 34 percent if you round up. Ignore the fact that four multiplied by one-fourth is one, not two. And the fact that services, of which America is a large exporter, are just ignored.

If you think looks suspiciously like Chat GPT math, you are probably correct. The administration claimed they were conducting detailed evaluations of trade barriers to U.S. goods in each country. But it’s clear that was a lie, and the White House scrambled after economist James Surowiecki reverse-engineered their fake reciprocal tariff rates.

A number of countries managed to escape these additional tariffs, primarily because of pre-existing trade deals or the lack of a bilateral trade surplus with the U.S. These include the United Kingdom, Australia, New Zealand, Singapore, and much of central and south America. Goods covered by the USMCTA deal are also exempt, but I doubt Canada and Mexico are taking much solace.

These tariffs, and their design, are terrible policy for three big reasons. First, balanced trade does not equal a stronger economy. International trade is well understood to be one of the driving forces behind rising prosperity and standards of living around the world. Trade allows countries to capitalize on their comparative advantage; they can produce what they are relatively best at, and end up with more total output and income. It also gives domestic firms a larger market. With more customers, they can take advantage of economies of scale. Finally, the competition leads to more choices and lower prices for consumers, pushing firms to innovate.

The United States has a trade deficit in goods because it is the richest country in the world and specializes in high-value, knowledge-intensive sectors. The trade imbalance in goods is an effect of economic prosperity, rather than a cause of economic malaise. About one-third of our exports are services, and the goods we do produce ourselves tend to be cutting edge and capital intensive, such as industrial machinery, medical devices, specialized electronics, and commercial aircraft/defense systems. We could produce all the inputs we need domestically, but we don’t because it is not the most efficient use of our workforce’s time. It would be like hiring Lebron James to do your taxes. Sure, he could do the job. But is that really the best use of his talent?

The second glaring weakness is expectations of “success” depend on assuming other countries, firms, and consumers won’t respond. A questionable assumption, at best. Countries up for a fight, like China, will retaliate directly, placing tariffs on American exports, further limiting the global market for our domestic firms. This will lead to further declines in output and employment, and concurrent increases in prices. As a result, the U.S. trade deficit - the difference between imports and exports, may not even decline! Even countries that don’t retaliate directly, like Vietnam, will learn a fundamental lesson: the United States cannot be trusted or relied upon. Policy makers around the world are already pivoting their economies to depend less on trade with the U.S. It may take a generation, and a sound repudiation of Trump in 2026 and 2028, for America to regain its standing on the world stage. But I believe we have passed the point of no return; these wounds may never completely heal. In no way is this development likely to promote economic prosperity in the U.S. or abroad.

I am not alone in this prediction. By Friday, the S&P 500 was down 17.6 percent from its recent peak just 6 weeks ago. By Monday, after a tweet falsely claiming Trump was considering a 90-day pause led to a chaotic rally and subsequent fall, a growing list of finance titans from Bill Ackman to Larry Fink to JP Morgan Chase CEO Jamie Dimon began publicly warning of the “economic nuclear winter” to come. Even Elon Musk joined the party, criticizing the tariffs and their chief architect,5 trade advisor Peter Navarro (along with Harvard, for good measure). Most importantly, regular Americans from across the political spectrum are starting to seriously worry about their jobs, finances, and futures.

The third major flaw of Trump’s tariffs is that neither he nor his advisors have clearly communicated what “success” is. Is it re-shoring manufacturing jobs like Trump says? Is it to lower trade barriers to U.S. firms around the world, like Treasury Secretary Scott Bessent says? Or is it to raise additional revenue to help pay down the national debt, as Peter Navarro says? None of these objectives are inherently bad. But any economic policy without a clear goal in mind is destined for failure.

What About the Jobs Report?

In last month’s post, I wrote the March jobs report would be the first reading we get on the labor market impact of Trump’s economic agenda. I expected to see a slowdown, especially in the federal government, but the numbers were decent on the surface, all things considered. Nonfarm payrolls grew by 228,000 over the month, and the unemployment rate held steady at 4.2 percent. Does this mean the U.S. economy is doing fine? Absolutely not. Job gains reflected idiosyncratic and temporary factors, or were concentrated in service sectors, like health care, where demand is relatively uncorrelated with trade policy. The employment change in January and February was also revised down by a combined 48,000 jobs. If I were a betting man, I would still expect the numbers to turn negative in the coming months, given Trump’s continued escalation of his trade war.

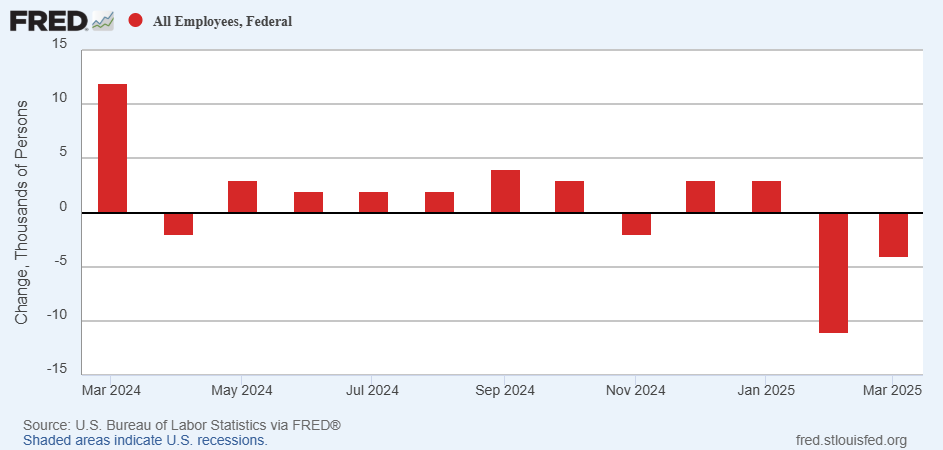

The March report showed an additional 5,000 lost jobs in the federal government compared to February.6 After reading so many heartbreaking LinkedIn posts from fired civil servants in recent weeks, I expected this number to be worse. It wasn’t because of a quirk of measurement. In the establishment survey - the Current Employment Statistics (CES) program - if you receive pay from an employer in the reference period7, you are counted as employed. This means that federal workers placed on paid administrative leave due to court orders, or those receiving severance pay, still count as employed. The former could account for between 16,000 and 24,000 workers. The Trump administration claims the latter includes up to 75,000, but the actual count is likely much less.

On a slightly optimistic note, I wrote on LinkedIn that federal layoffs gave state and local governments a unique chance to attract highly skilled, experienced, and mission-driven workers. If cities and states step up hiring, then negative labor market impacts could be mitigated. In March, state and local employment rose by 23,000.

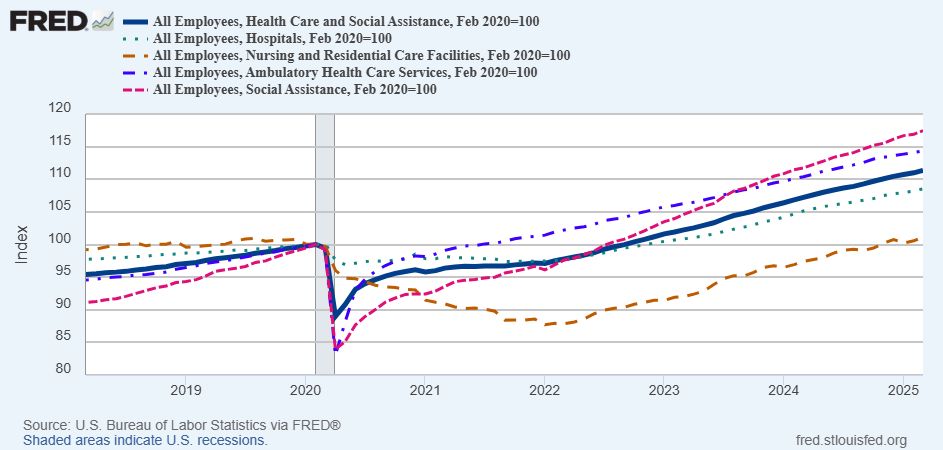

The leading sectors, however, were health care and social assistance. Health care includes establishments providing medical, diagnostic, and treatment services such as hospitals, physician offices, nursing care facilities, and home health care. Social assistance - a closely related sector - provides mostly non-medical services to families in need, like child care, food and housing support, vocational rehabilitation, and help for the elderly and disabled.

The health care sector added 54,000 jobs in March, on par with its average monthly gain since 2022. Growth was evenly split between hospitals, ambulatory health care services8, and nursing and residential care facilities, with all three sectors adding between 17,000 and 20,000 jobs. Social assistance employment rose by 24,000, almost entirely in individual and family services.

It is important to note these sectors have all been growing at strong rates for a number of years, even outpacing their pre-COVID growth. The primary factors have been an aging population, an increased prevalence of chronic conditions, and an increased focus on mental health services. While demand for these services is likely inelastic, and won’t shift dramatically in response to trade policy, it’s unrealistic to expect these sectors to carry the U.S. economy on their own.

Retail trade (+24,000) also had a strong March, but this too was driven by a one-off event. From February 6 to 17, about 10,000 United Food and Commercial Workers (UFCW) members from 79 locations of Kroger-owned and Colorado-based supermarket chain King Soopers went on strike in response to alleged unfair labor practices and for better pay. After twelve days, which closely aligned with February’s reference period, the two sides reached a return-to-work agreement. Lo and behold, in March, employment in food and beverage retailing rebounded strongly compared to February.9

Transportation and warehousing also outperformed expectations, adding 23,000 jobs, primarily among couriers and messengers (+16,000) and in truck transportation (+10,000). However, this likely reflected a mad dash by businesses to stockpile goods before Trump’s tariffs take effect. Not exactly sustainable. Meanwhile, employment in the U.S. manufacturing sector was essentially unchanged.

-Evan

For example, Peter Heather, writing in The Fall of the Roman Empire, writes, “The Roman Empire had sown the seeds of their own destruction.” in Chapter 10.

I swear I’m not one of those guys who is irrationally obsessed with the Roman Empire. I’ve just been slowly listening to the incredibly long, detailed, and wonderful The History of Rome podcast by Mike Duncan for the past eighteen months.

It is embarrassing not because it is simple, but because it has no sound basis in economic theory. As an aside, the OTR document is one of the most terrible economic policy discussions I have ever read. Every American economist should be personally ashamed that this type of analysis is driving our trade policy.

Epsilon stands for the elasticity of import demand with respect to prices, while varphi is the elasticity of import prices with respect to tariffs. Don’t worry about it too much. If you want to worry about it, I encourage reading the Tax Foundation’s unnecessarily detailed but exceptional discussion.

I think architect is giving him too much credit.

February’s estimate was revised down by 1,000, while federal employment declined by an additional 4,000 in March.

The pay period encompassing the 12th day of the month.

In this context, ambulatory means “able to walk”, not using an ambulance. Thus, ambulatory health care services includes offices of physicians, dentists, optometrists, outpatient care centers, and other medical and diagnostic labs.

Researching this strike led me to the awesome Labor Action Tracker maintained by the Schools of Labor Relations at Cornell University and the University of Illinois. I sense another post about the geographic concentration of strikes in my future.